The Macro Sphere

Stem the fall, but how? – The Past Playbook & The Way Ahead

History might not repeat itself, but it often rhymes.

In this note, we review the past episodes of steep pressure on the currency and the policy response therein to arrest the fall in the currency. The focus is on three key episodes over the last ~15 years and the possible policy options.

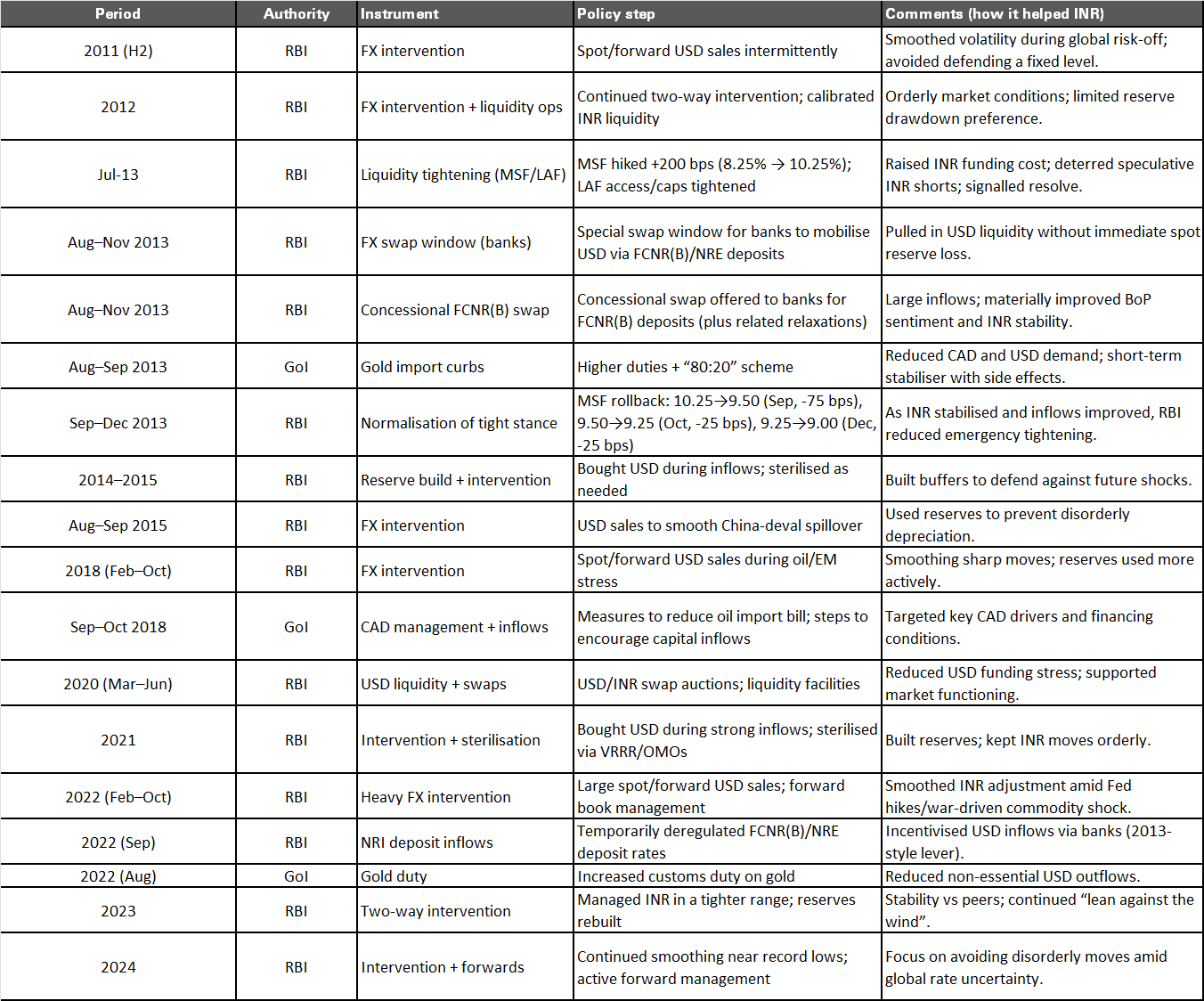

Most of these measures were undertaken in 2013 to stem the Rupee fall which swiftly dropped to 68USD from 55USD. However, at that time India faced a massive twin-deficit problem which had exacerbated the depreciation. The macro dynamics as well as global drivers were far more different than they are today for India. The period of 2013 was far more painful. India’s net oil bill was 5.5 per cent of GDP and the CAD was 4.3 percent on average in FY12-FY13, with a BoP of -0.3 per cent in the said period. During this period, to tackle the twin deficits, on the fiscal front, the govt. raised gold import duty and removed fuel subsidies and deregulated fuel prices; and, to manage the BoP situation, the RBI raised overnight rates, tightened liquidity conditions and announced a swap window facility for the banks to raise dollar deposits (see Table 3).

This time around, India’s macro standing is far stronger – esp. on the twin deficits. The capital account inflows & surplus have been a key concern this time around, as dollar inflows have dried up.

Also, this time the global backdrop is significantly different from the past episodes as it follows a war in the Middle East – supply, production, and logistics for almost all energy products wrapped all in one – which makes the current situation far more precarious from an oil prices standpoint and, consequently, for the macroeconomic implications for India.

While India still remains energy dependent, the duration of the impact could turn out to be a bigger drag than the CAD or BoP situation as these dynamics have changed over the years. As of today, India’s CAD is at 0.4 per cent of GDP (CY25), but capital outflows have led to a BoP deficit of 0.6 per cent of GDP (CY25). In terms of net oil imports, the same is at 3 percent of GDP (2ppts lower than FY13) and net services exports at 4.8 per cent of GDP (1 ppt higher than FY13). The price sensitivity to petroleum products remains a key risk to the CAD, even as the BoP dynamics have evolved.

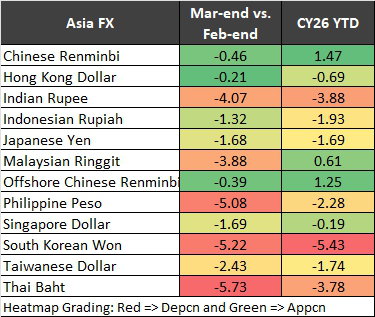

Since the Middle East war broke out, unlike the 2013 taper tantrum phase; and unlike the Russia-Ukraine conflict – the current situation is far more different. Consequently, the currency pressures have been a global phenomenon esp. in Asian economies (see Table 1) - which are on the receiving end of the production-and-supply shocks of the energy economy. While some signs of an end are making the headlines, no immediate end is in sight; in the past few days, several EM countries have refrained from aggressive intervention and are tackling the situation by taking other measures.

In the current context, what options do the policymakers have, this time around? Could the past playbook be used again?

Fiscal measures: India has taken the fiscal route to absorb the shock by lowering indirect taxes on automobile fuel and in order to incentivize domestic fuel supply, raised windfall taxes. The estimated impact from fuel tax cuts stands at INR 1.5-2.0 lakh crore. However, a part of this cost is expected to get addressed by the increased windfall taxes, which assuming oil exports stay flat, gives fiscal gains of ~INR 1 lakh crore. Consequently, the net fiscal impact is reduced to ~INR 700-900 billion; translating into 0.2-0.3 per cent of GDP. In latest developments, the govt. has increased prices on aviation fuel and commercial gas (LPG), signaling that higher prices may get passed-on. Due to natural gas issues, any increase in fertilizer costs is likely to get absorbed by the govt. further adding to fiscal costs in the form of subsidy. The additional impact from fertilizer subsidy is estimated to be 0.3 per cent of GDP.

Meanwhile, the immediate impact is visible via the currency channel owing to dollar demand.

RBI measures: The RBI has intervened in the FX market, however, on 27th March it stepped up its defense, and rolled out a measure to curb speculation after it slid to a new low amid concerns of a widening trade gap driven by the US-Iran war. The RBI directed banks to keep their net open position (NOP) in INR in the onshore deliverable market within 100USD million at the end of each business day amid rising volatility in the FX market – which is due to come into effect from 10-April. While at the open on Monday, the INR swung into the green, increased dollar demand again led to a weak close. Observing this, on a FX & rates market bank holiday, the RBI announced another measure to clamp down on speculative activities.

The RBI restricted banks from offering rupee non-deliverable forwards to any clients and barred the rebooking of cancelled contracts, reportedly disrupting a 149USD billion-a-day market1. The RBI took another stern step after its initial attempt to stabilise the currency was undermined by banks and corporates exploiting an arbitrage opportunity. The Rupee surged the most in 12 years on 2-April, as currency trading resumed after a two-day holiday break. It gained almost 2 per cent to 93.14USD (around noon on 2-Apr), after having traded at an all-time low above the 95-per dollar level on 30-March, the first trading day after the NOP measures were announced. Apparently, a similar strategy of NOP was deployed in December 2011.

The Way Ahead:

Govt. policy, fiscal levers:

Expenditure pruning: After fuel tax cuts, the fiscal levers are limited. Given that ~68 per cent of the Centres’ Revenue expenditure is committed or recurring in nature, the room to prune/ration spending is rather limited. This could either mean reduced capital account spending or a higher fiscal deficit. For now, the govt. has reduced the net fiscal impact.

Incrementally, a portion of the surge in oil prices could be passed on to the consumers if the duration of the war were to last longer, while subsidizing fertilizer.

Amid the supply shock with the Strait of Hormuz being closed, the effort to procure and source oil & gas from other countries - something that the govt. is actively doing - should help keep the economic engines running without significant fiscal & economic costs.

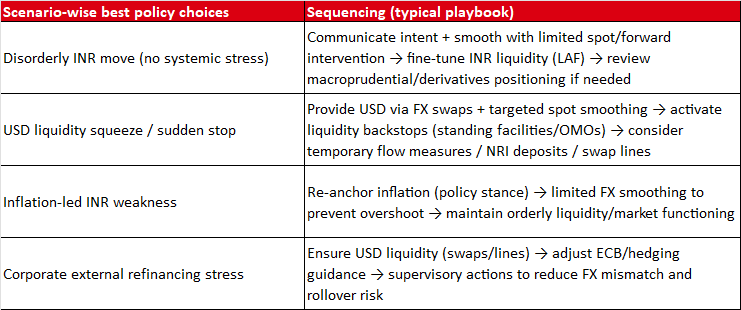

RBI’s policy options: The RBI does have a range of policy instruments in its toolkit to manage the external sector headwinds, however, the effectiveness of each entails a cost.

One past policy measure that brings up nervousness is that of the hike in overnight rates. In 2013, the RBI’s Rupee “defence” move was a +200 bps spike in overnight rates followed by attracting long term dollar deposits. The overnight rate hikes were then reversed. While this option is also available with the RBI, at this juncture, it does not appear to be the case.

From the other measures, whether the RBI opts for macroprudential adjustments, liquidity tightening or money market ops, FX intervention, FX regulations or FX inflow mobilization remains to be seen contingent upon the evolving war conditions and its implications on domestic macros (Table 2).

The RBI’s recent NOP measure was one such policy tool that was deployed to counter speculative moves on the INR; and it could possibly step up its measures along these lines. The other measures from its toolkit - as laid out in Table 1 could be - FX swap or swap line like measures; restrictions on outward remittances, or outward foreign direct investments (which have been one of the major reasons behind weaker Net FDI flows). The RBI could also offer banks incremental benefits on FX NRI deposits (something observed during 2022-2023).

All-in-all, the policy choices and responses this time around could be somewhat different given the global developments as well as India’s changed BoP dynamics. There are no set rules and the RBI does have a slew of policy tools up its sleeve and at its disposal, the point is when and what is deployed will be contingent upon the source of the external headwind.

Policy reforms to attract long term capital are the most efficient, but likely to be slower in response. For instance, the relaxations in ECB norms, and the govt. directive on FDI rules on Chinese investments are some of the most recent changes.

The RBI MPC meets on 8th April and the focus will be on its assessment of the current situation as well as its preparedness to tackle the uncertainty.

Table 1: One-month into ME war, all of Asia FX on a weaker footing

Click the image to enlarge

Source: Bloomberg as of 2-Apr, 11:00 AM IST

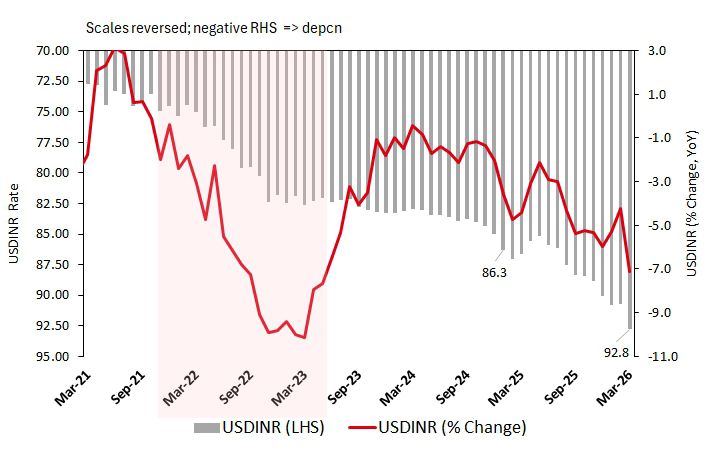

Chart 1: USDINR depcn rate still not as bad as CY22

Click the image to enlarge

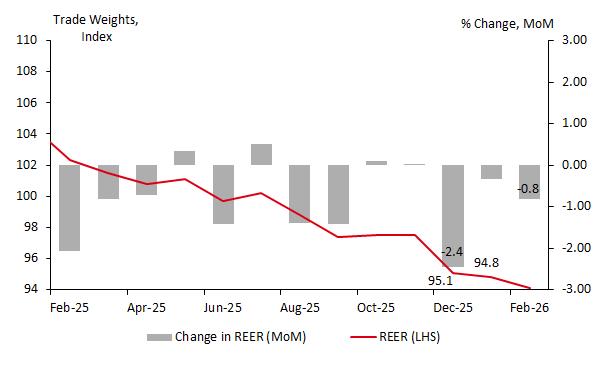

Chart 2: In REER terms, currency at decadal lows

Click the image to enlarge

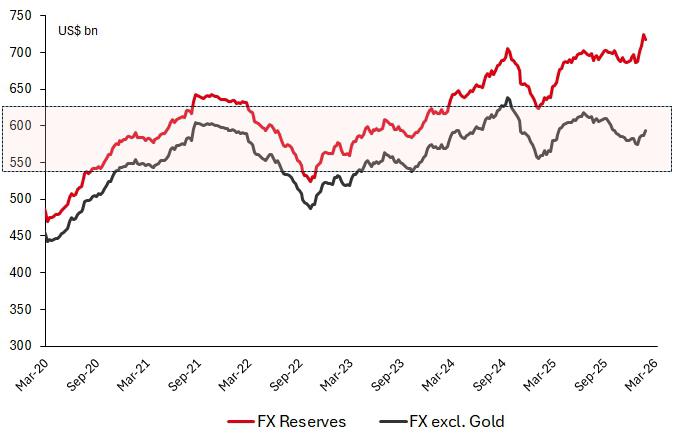

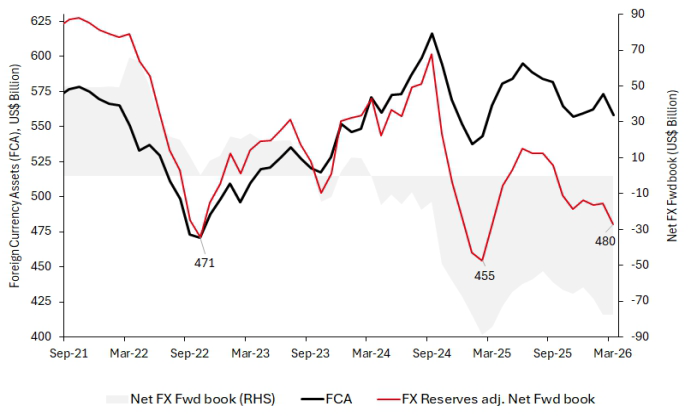

Chart 3: India FX Reserves near 700USD billion; FX Reservesexcl. gold is range bound...

Click the image to enlarge

Chart 4: ...within FX, the Foreign Currency Assets (FCA) and FCA adj. for forward book dwindles

*Note: for Mar'26 FCA data till 20-March and Fwd. book data is till Feb

Click the image to enlarge

Table 2: No set rules: A range of policy tools at its disposal – when and what is deployed is contingent upon the source of external headwinds

Click the image to enlarge

Table 3: In the recent past: The measures RBI/GoI undertook to stem the Rupee fall. What options does it have this time? Could the past playbook be used again?

Click the image to enlarge

Source: Bloomberg, CMIE Database, RBI Notifications, HSBC AMC FI, Econ Desk

Conclusion: India’s INR stress is being driven less by 2013-style twin-deficit fragility and more by a global energy shock and weaker capital inflows (amid global uncertainty and US trade tariffs), shifting the pressure point from the current account to the capital account/BoP – which allows a response that is more targeted, less growth-damaging, maintains India’s credibility and overall, may not exactly replicate the 2013 playbook. For the RBI, the priority is to preserve market functioning and deter one-way speculation through prudential limits (NOP/NDF measures), liquidity/market operations and calibrated FX intervention to smooth volatility, especially as usable reserve firepower is lower than headline numbers imply: while FX reserves were 728USD billion, FCA at 573USD billion (end-Feb), and adjusting for the RBI’s net forward dollar book (Feb) takes effective FCA to ~495USD billon; Now, if we take the Feb’s forward book size of 78USD billion on 20th March FCA levels, the adj. FCA is even lower at USD480 billion– making a stronger case for a more calibrated & judicious intervention. If pressures persist, a more likely measure is inflow mobilization, swap-style facilities, improved terms for NRI deposits, and incremental reforms to attract longer-term capital (e.g., ECB/FDI easing) - rather than aggressive policy/liquidity tightening. Broad capital controls, particularly restrictions on foreign investors or FPI repatriation, remain unlikely and would be a last resort given India’s credibility and market-access priorities; consistent with 2013/2020/2022, policymakers are more likely to pull dollars in than to restrict outflows. Overall, the most credible path to ‘stem the fall’ is a two-track approach: near-term stabilisation via targeted prudential/market measures and selective FX operations, alongside steps to mobilise durable dollar inflows - while avoiding heavy-handed controls that could undermine confidence.

Ref Note 1: Bloomberg article dated 2-Apr titled Forex War: How RBI’s USD149 billion crackdown is stopping speculators from falling rupee

Past performance may or may not be sustained in future and is not a guarantee of any future returns.

Source – RBI, RBI Database, CMIE, Bloomberg, HSBC Research AMC, Fixed Income. Data as on April 2, 2026.

Note: Views provided above are based on information in public domain and subject to change. Investors are requested to consult their financial advisor for any investment decisions.

Disclaimer: This document has been prepared by HSBC Asset Management (India) Private Limited (HSBC) for information purposes only and should not be construed as i) an offer or recommendation to buy or sell securities, commodities, currencies or other investments referred to herein; or ii) an offer to sell or a solicitation or an offer for purchase of any of the funds of HSBC Mutual Fund; or iii) an investment research or investment advice. It does not have regard to specific investment objectives, financial situation and the particular needs of any specific person who may receive this document. Investors should seek personal and independent advice regarding the appropriateness of investing in any of the funds, securities, other investment or investment strategies that may have been discussed or referred herein and should understand that the views regarding future prospects may or may not be realized. In no event shall HSBC Mutual Fund/HSBC Asset management (India) Private Limited and / or its affiliates or any of their directors, trustees, officers and employees be liable for any direct, indirect, special, incidental or consequential damages arising out of the use of information / opinion herein. This document is intended only for those who access it from within India and approved for distribution in Indian jurisdiction only. Distribution of this document to anyone (including investors, prospective investors or distributors) who are located outside India or foreign nationals residing in India, is strictly prohibited. Neither this document nor the units of HSBC Mutual Fund have been registered under Securities law/Regulations in any foreign jurisdiction. The distribution of this document in certain jurisdictions may be unlawful or restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions. If any person chooses to access this document from a jurisdiction other than India, then such person do so at his/her own risk and HSBC and its group companies will not be liable for any breach of local law or regulation that such person commits as a result of doing so.

Document intended for distribution in Indian jurisdiction only and not for outside India or to NRIs. HSBC MF will not be liable for any breach if accessed by anyone outside India. For more details, click here / refer website. click here / refer website.

© Copyright. HSBC Asset Management (India) Private Limited 2026, ALL RIGHTS RESERVED

HSBC Mutual Fund, 9-11th Floor, NESCO - IT Park Bldg. 3, Nesco Complex, Western Express Highway, Goregaon East, Mumbai 400063. Maharashtra. GST -27AABCH0007N1ZS | Website: www.assetmanagement.hsbc.co.in.www.assetmanagement.hsbc.co.in.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

CL 3912