Compelling valuations emerge after recent market corrections

Recent market movements have led to a meaningful correction across market segments. When we look at the data over the last three calendar years, the adjustment is evident not just in prices but also through a phase of market consolidation, which together is helping bring valuations closer to long-term averages.

Price adjustments across market segments

Small and mid-cap indices have witnessed deeper corrections compared to large caps.

BSE Small Cap index has corrected from a high of 57,827 in 2024 to around 45,225 in 2026, a decline of nearly 22 per cent from peak levels.

Click the image to enlarge

BSE Mid Cap index has moved from a high of 49,701 in 2024 to about 42,138 in 2026, reflecting a correction of nearly 15 per cent from peak levels.

Click the image to enlarge

The BSE Sensex, after touching an all-time high of ~86,000 in 2025, is currently around 74,500, representing a correction of roughly 13–14 per cent from peak levels.

Click the image to enlarge

Source – BSE India. Period under consideration for all three indices is Jan 1, 2024 to March 20, 2026. “Open” represents the index level on Jan 1 of the respective year. “High” and “Low” represent the highest and lowest levels recorded during the year. “Close” represents Dec 31 for 2024 and 2025, while the closing level for 2026 is March 20, 2026. Past performance may or may not be sustained in the future.

Such adjustments across segments have helped cool off elevated valuations that had built up during the previous rally.

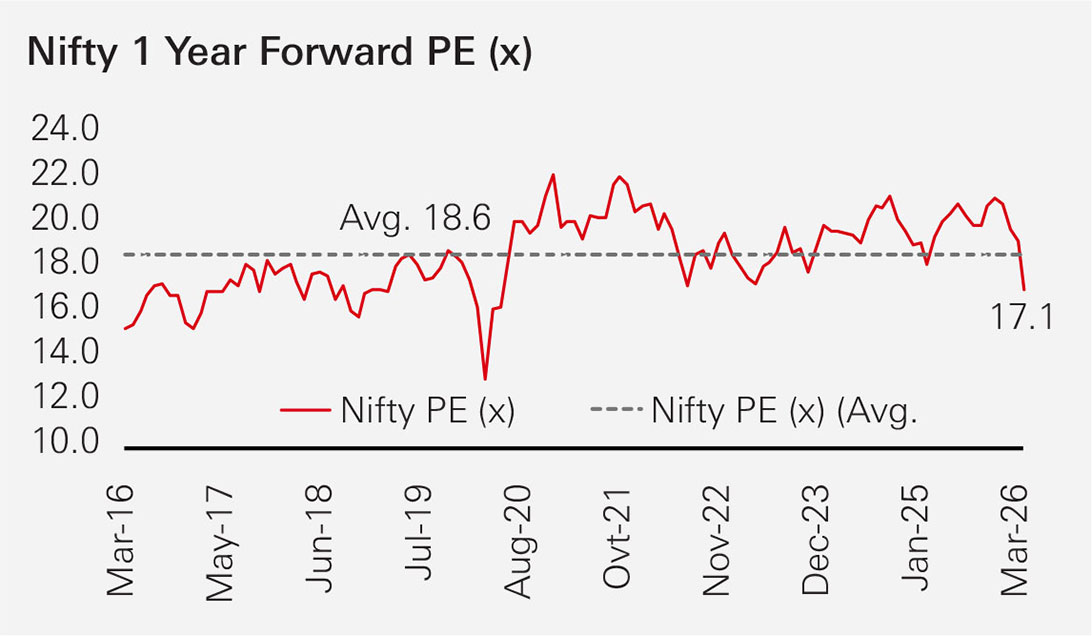

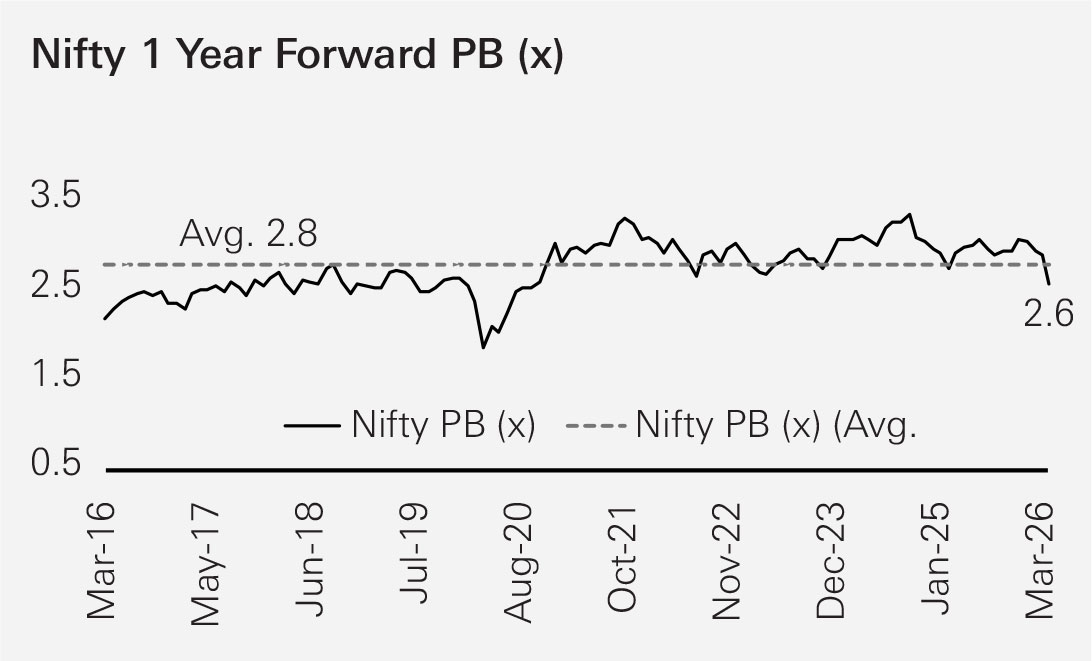

Valuations moving closer to long-term averages

The recent phase of market correction has not only adjusted prices but has also helped moderate valuation multiples across the market.

Click the image to enlarge

Click the image to enlarge

As of 23 March 2026, the Nifty 50 is trading at a 1-year forward Price-to-Earnings (P/E) multiple of around 17.1x, which is below its long-term average levels, indicating a meaningful cooling in valuations compared to the earlier phase of the rally.

Similarly, the Price-to-Book (P/B) ratio stands at around 2.6x, also trending close to historical averages. This moderation reflects how the recent consolidation phase has helped normalise valuations that had become elevated during the previous market upcycle.

In essence, the market has witnessed both price correction and valuation normalisation, bringing valuations closer to more sustainable levels. Historically, such phases have often created attractive opportunities for long-term investors to gradually build exposure to equities through disciplined investment approaches.

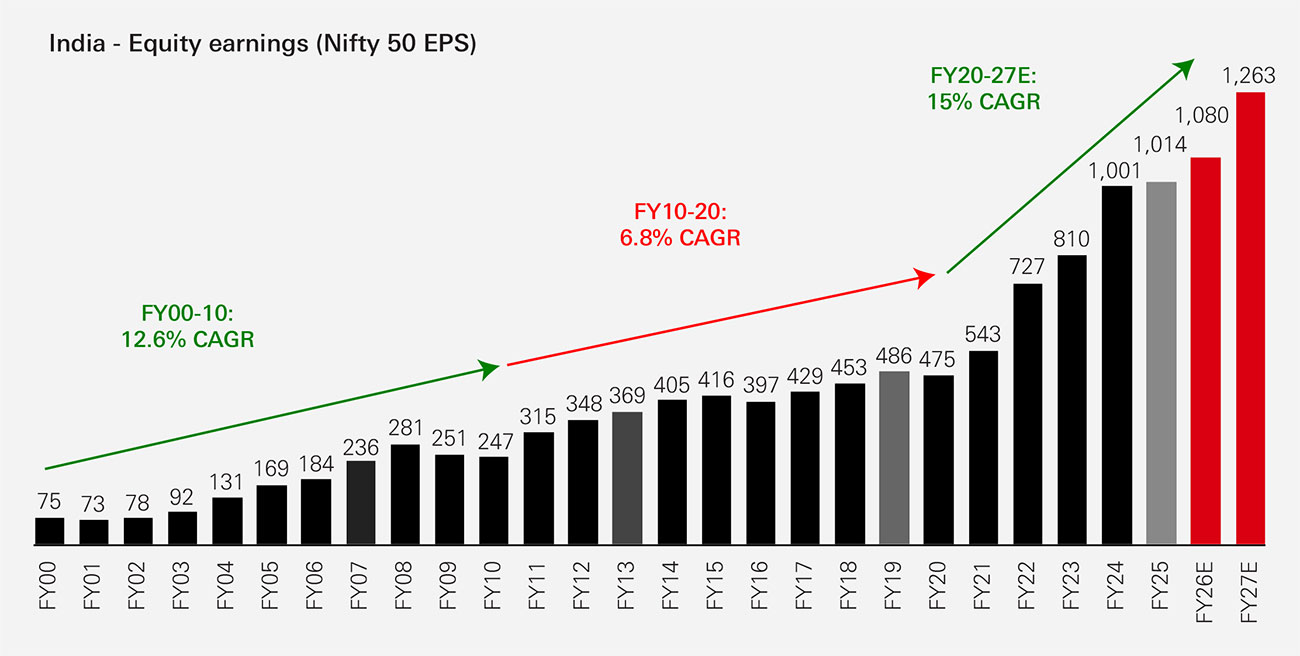

Earnings growth outlook remains supportive

While valuations have moderated following the recent market correction, the earnings outlook for Indian corporates continues to remain encouraging.

Historical data shows that corporate earnings growth has evolved across different phases. Between FY00–FY10, Nifty 50 earnings grew at a CAGR of around 12.6 per cent, followed by a relatively slower phase of ~6.8 per cent CAGR between FY10–FY20.

Earnings trend

Click the image to enlarge

Source: MOSL, Bloomberg, Data as on 27 February 2026. Past performance may or may not be sustained in future and is not a guarantee of any future returns. Note: The details provided above is as per the information available in public domain at this moment and subject to change. Please consult your financial advisor for any investment decisions.

However, the earnings cycle has improved meaningfully in recent years. Estimates indicate that Nifty 50 earnings are expected to grow at around 15 per cent CAGR between FY20 and FY27, reflecting stronger corporate balance sheets, improved profitability and sustained economic momentum.

This improving earnings trajectory suggests that the recent market consolidation has occurred at a time when the earnings cycle remains supportive, which could help justify valuations over the medium to long term.

What does this mean for investors?

For long-term investors, periods of market consolidation have often been opportunities rather than setbacks.

Instead of attempting to time the exact market bottom, investors may consider:

- Continuing Systematic Investment Plans (SIPs)

- Deploying idle money gradually through Systematic Transfer Plans (STPs)

- Staying invested to benefit from rupee cost averaging during volatility

Periods of volatility help investors accumulate more units at relatively lower prices, potentially improving long-term outcomes when markets recover

The bottom line

Market adjustments are an inherent part of the equity journey. While volatility may create short-term discomfort, it often lays the foundation for future opportunities

With valuations becoming more reasonable after both price corrections and a consolidation phase, the current environment could present attractive entry levels for investors with a long-term horizon.

The message remains consistent: Stay disciplined, stay invested and use volatility as an opportunity rather than a deterrent.

Views provided above are based on information in public domain and subject to change. Investors are requested to consult their financial advisor for any investment decisions. Past performance may or may not be sustained in future and is not a guarantee of any future returns

Source: Bloomberg, BSE, NSE, MOSL & HSBC MF estimates as on March 23, 2026 end or as latest available

Disclaimer - This document has been prepared by HSBC Asset Management (India) Private Limited (HSBC) for information purposes only and should not be construed as i) an offer or recommendation to buy or sell securities, commodities, currencies or other investments referred to herein; or ii) an offer to sell or a solicitation or an offer for purchase of any of the funds of HSBC Mutual Fund; or iii) an investment research or investment advice. It does not have regard to specific investment objectives, financial situation and the particular needs of any specific person who may receive this document. Investors should seek personal and independent advice regarding the appropriateness of investing in any of the funds, securities, other investment or investment strategies that may have been discussed or referred herein and should understand that the views regarding future prospects may or may not be realized. In no event shall HSBC Mutual Fund/HSBC Asset management (India) Private Limited and / or its affiliates or any of their directors, trustees, officers and employees be liable for any direct, indirect, special, incidental or consequential damages arising out of the use of information / opinion herein. This document is intended only for those who access it from within India and approved for distribution in Indian jurisdiction only. Distribution of this document to anyone (including investors, prospective investors or distributors) who are located outside India or foreign nationals residing in India, is strictly prohibited. Neither this document nor the units of HSBC Mutual Fund have been registered under Securities law/Regulations in any foreign jurisdiction. The distribution of this document in certain jurisdictions may be unlawful or restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions. If any person chooses to access this document from a jurisdiction other than India, then such person do so at his/her own risk and HSBC and its group companies will not be liable for any breach of local law or regulation that such person commits as a result of doing so

Investors are requested to note that as per SEBI (Mutual Funds) Regulations, 1996 and guidelines issued thereunder, HSBC AMC, its employees and/or empaneled distributors/agents are forbidden from guaranteeing/promising/assuring/predicting any returns or future performances of the schemes of HSBC Mutual Fund. Hence please do not rely upon any such statements/commitments. If you come across any such practices, please register a complaint via email at investor.line@mutualfunds.hsbc.co.in.

The above information is for illustrative purposes only. The sector(s) mentioned in this document do not constitute any research report nor it should be considered as an investment research, investment recommendation or advice to any reader of this content to buy or sell any stocks / investments

Document intended for distribution in Indian jurisdiction only and not for outside India or to NRIs. HSBC MF will not be liable for any breach if accessed by anyone outside India. For more details, click here / refer website.

© Copyright. HSBC Asset Management (India) Private Limited 2026, ALL RIGHTS RESERVED.

HSBC Mutual Fund, 9-11th Floor, NESCO - IT Park Bldg. 3, Nesco Complex, Western Express Highway, Goregaon East, Mumbai 400063. Maharashtra.

GST - 27AABCH0007N1ZS | Website: www.assetmanagement.hsbc.co.in

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.