CEO Speak March 2026

The month of March has been marked by heightened uncertainty in global financial markets, largely influenced by geopolitical developments in West Asia. Such events tend to create sharp reactions across asset classes, often leading to volatility in equity, currency, and commodity markets. While these developments can be unsettling, it is important for investors to interpret them with perspective rather than panic.

Correction Unlocks Valuation Comfort

Historically, geopolitical tensions have led to temporary disruptions in financial markets. Markets tend to react swiftly to uncertainty, but they also stabilise as clarity emerges. Over time, economic growth, business performance, and policy direction regain focus as the primary drivers of market returns.

Over the past three years, a mix of price correction and consolidation has helped bring market valuations closer to long-term averages, making them more reasonable for investors.

- BSE Small Cap index has corrected from a high of 57,827 in 2024 to around 45,225 in 2026, a decline of nearly 22 per cent from peak levels

- BSE Mid Cap index has moved from a high of 49,701 in 2024 to about 42,138 in 2026, reflecting a correction of nearly 15 per cent from peak levels

- The BSE Sensex, after touching an all-time high of ~86,000 in 2025, is currently around 74,500, representing a correction of roughly 13–14 per cent from peak levels

Source – BSE India. Period under consideration for all three indices is Jan 1, 2024 to March 20, 2026.Past performance may or may not be sustained in the future.

These are healthy adjustments following periods of strong rally and elevated expectations.

India’s Structural Strength Remains Intact

India’s medium- to long-term growth drivers remain stable. Domestic demand, infrastructure development, and policy continuity continue to support the broader economic outlook.

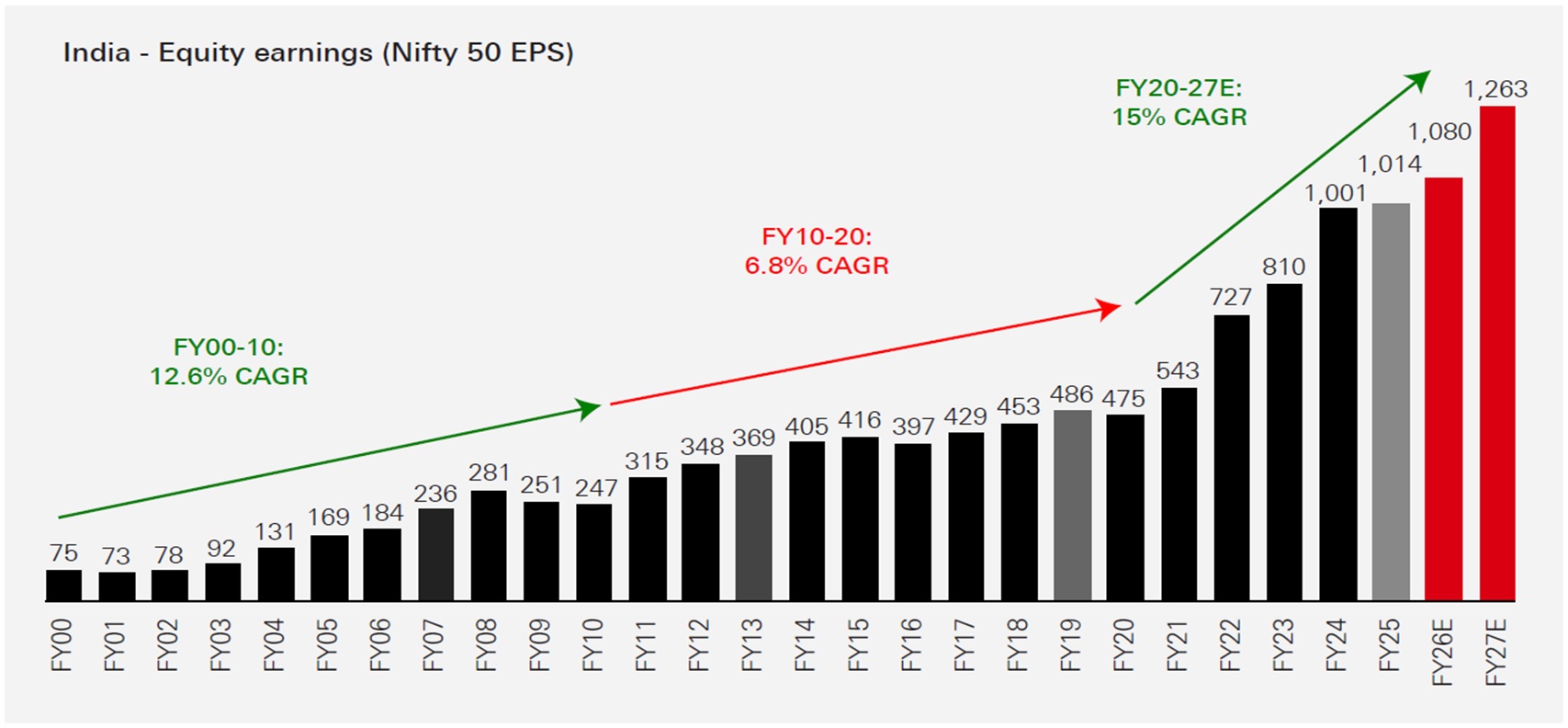

A strengthening earnings cycle continues to provide an important anchor for markets, with Nifty 50 earnings estimated to grow at ~15 per cent CAGR between FY20 and FY27, supported by healthier balance sheets, improved profitability, and sustained economic momentum. This suggests that the recent market consolidation is occurring alongside robust earnings growth, which can help support valuations over the medium to long term.

Earnings trend

Source: MOSL, Bloomberg, Data as on 27 February 2026. Past performance may or may not be sustained in future and is not a guarantee of any future returns.

Note: The details provided above is as per the information available in public domain at this moment and subject to change. Please consult your financial advisor for any investment decisions.

For investors, such phases have historically presented opportunities rather than setbacks—making it prudent to stay invested, continue SIPs, and gradually deploy surplus funds through STPs to potentially benefit from volatility-led averaging.

It is important to remember:

- Markets have navigated geopolitical uncertainties or events in the past

- Sharp corrections are often followed by swift recoveries

- Missing the recovery phase can significantly impact long-term returns

The Way Forward for Investors

At HSBC Mutual Fund, we continue to believe and advise that the most effective investment behaviour is often the simplest:

- Stay aligned to your long-term financial goals

- Maintain asset allocation discipline

- Avoid making reactive decisions based on short-term developments

As investors, our strength lies not in predicting every market movement, but in staying committed to a disciplined investment approach.

Remain patient. Remain invested. And most importantly, remain confident in the long-term journey.

Views provided above are personal and based on information in public domain and subject to change. Investors are requested to consult their financial advisor for any investment decisions.

Source: AMFI, BSE, HSBC MF Research. Data as on March end, 2026 or as latest available

Disclaimer: This document has been prepared by HSBC Asset Management (India) Private Limited (HSBC) for information purposes only and should not be construed as i) an offer or recommendation to buy or sell securities, commodities, currencies or other investments referred to herein; or ii) an offer to sell or a solicitation or an offer for purchase of any of the funds of HSBC Mutual Fund; or iii) an investment research or investment advice. It does not have regard to specific investment objectives, financial situation and the particular needs of any specific person who may receive this document. Investors should seek personal and independent advice regarding the appropriateness of investing in any of the funds, securities, other investment or investment strategies that may have been discussed or referred herein and should understand that the views regarding future prospects may or may not be realized. In no event shall HSBC Mutual Fund/HSBC Asset management (India) Private Limited and / or its affiliates or any of their directors, trustees, officers and employees be liable for any direct, indirect, special, incidental or consequential damages arising out of the use of information / opinion herein.

This document is intended only for those who access it from within India and approved for distribution in Indian jurisdiction only. Distribution of this document to anyone (including investors, prospective investors or distributors) who are located outside India or foreign nationals residing in India, is strictly prohibited. Neither this document nor the units of HSBC Mutual Fund have been registered under Securities law/Regulations in any foreign jurisdiction. The distribution of this document in certain jurisdictions may be unlawful or restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions. If any person chooses to access this document from a jurisdiction other than India, then such person do so at his/her own risk and HSBC and its group companies will not be liable for any breach of local law or regulation that such person commits as a result of doing so.

The above information is for illustrative purposes only. The sector(s) mentioned in this document do not constitute any research report nor it should be considered as an investment research, investment recommendation or advice to any reader of this content to buy or sell any stocks / investments.

© Copyright. HSBC Asset Management (India) Private Limited 2026, ALL RIGHTS RESERVED. All third party trademarks (including logos and icons) remain the property of their respective owners. Use of it does not imply any affiliation with or endorsement by them.

HSBC Mutual Fund, 9-11th Floor, NESCO - IT Park Bldg. 3, Nesco Complex, Western Express Highway, Goregaon East, Mumbai 400063. Maharashtra.

GST - 27AABCH0007N1ZS | Website: www.assetmanagement.hsbc.co.in

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

CL 3914

![]() To Transact on WhatsApp – Send us “Hi” on 9326929294 TnC

To Transact on WhatsApp – Send us “Hi” on 9326929294 TnC

![]() For Product updates on WhatsApp – Send us “Hi” on 8879900800

TnC

For Product updates on WhatsApp – Send us “Hi” on 8879900800

TnC

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.